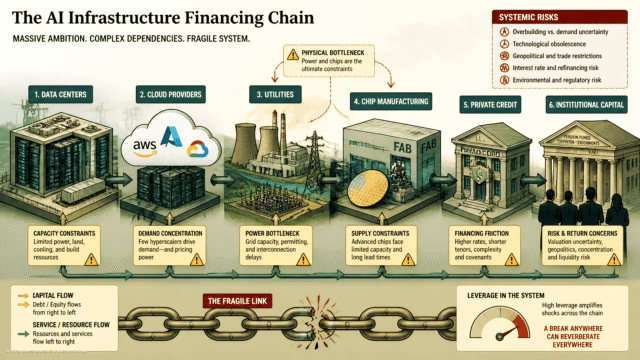

The Rotation Everyone’s Watching

Samsung’s earnings were, by most accounts, very good—just not good enough to sustain the narrative that memory chip demand is an infinite escalator. When the stock dropped 7%, it dragged down other hardware names like Micron. Observers noted that investors quickly extrapolated the results across the entire AI infrastructure theme.

What happened next was the real story. Capital didn’t flee tech. It shifted sideways into the megacap platforms that have spent much of the year in the penalty box: Amazon, Alphabet, Meta, Apple, and even Nvidia itself. Enterprise software names like Salesforce, Adobe, and ServiceNow also caught a bid.

The message seemed to be: the hardware layer is getting crowded, and the software layer might finally be due for a re-rating.

When Hardware Steals the Spotlight (and Then Gives It Back)

For more than a year, the AI conversation has been dominated by the physical layer. Nvidia’s GPUs, memory chips, and the data center buildout became the headline act. That made sense when the bottleneck was compute. But markets are fickle teachers. They reward what’s scarce, and they punish what gets too popular.

Samsung’s stumble may have been the first clear signal that the AI supply chain trade is no longer starved for attention or capital. If memory chip demand is even slightly in question, the whole “constrained supply” thesis gets a haircut. Suddenly, the companies that pay for all those chips—the ones actually building AI-powered products—start to look like the smarter bet.

What This Means for the AI Tools You Actually Use

For anyone comparing AI tools, the rotation is a reminder that the real leverage in AI is moving up the stack. The hardware layer is essential, but it’s increasingly commoditized. The differentiation, the moats, and the user-facing value live in the platforms and applications.

When Amazon and Alphabet surge, they’re not just idle stock tickers. They’re the hosts of AWS and Google Cloud, the home of Vertex AI, Bedrock, and a growing fleet of managed AI services. A revival in these stocks suggests that the market believes the cloud platforms—and by extension, the tools built on top of them—will capture more of the AI value chain.

What about the tools? The shift could mean:

- AI platform pricing stabilizes as cloud providers regain confidence.

- More investment flows into application-layer AI rather than pure infrastructure.

- The bar for AI tool claims rises—investors (and users) will scrutinize whether a tool actually solves a problem or just consumes GPUs.

For the founders and marketers reading this, the takeaway is clear: if your AI tool’s narrative is all about the model size and not about the workflow outcome, it’s time to rewrite the deck.

The Megacap Comeback: Platforms Over Picks and Shovels

The return of the big tech names isn’t just nostalgia for the old FAANG days. It’s a re-evaluation of who controls the AI distribution. Amazon, Google, and Meta have spent months getting beaten up while Nvidia stole the show. Now, with hardware sentiment cooling, the platforms that serve millions of developers and businesses are back in favor.

And it’s not just the cloud hyperscalers. Enterprise software companies like Salesforce and Adobe are integrating AI so deeply into everyday workflows that they’re becoming the default AI interfaces for the non-technical workforce. The market’s nod to those names is a signal that the AI tools ecosystem is shifting from the “what” (the raw technology) to the “how” (the embedded experience).

That’s a healthier dynamic for AI adopters. When the money flows toward the application layer, you get better integrations, more reliable APIs, and tools that feel less like science experiments and more like software.

How to Read the Shift Without a Bloomberg Terminal

You don’t need to track tick-by-tick moves to notice what’s changing. Watch for a few patterns:

- Hardware-obsessed headlines fade. When the daily AI news stops leading with chip shipment numbers and starts leading with product launches, the rotation is real.

- Cloud AI services announce fewer “coming soon” features and more GA releases. That’s a sign that investments are translating into usable tools.

- AI tool marketplaces become noisier. More capital into the application layer means more startups, more comparisons, more noise. The ability to filter effectively becomes a superpower.

That last point is where AiToolsObserver sits. We’re not here to pick stocks; we’re here to help you pick the right AI tool when the market gets crowded. And right now, the signals suggest it’s about to get much more crowded.

What to Do with This

The Samsung earnings event isn’t a buy or sell signal for your tool stack. It’s a reminder that the AI economy is still finding its balance. When the hardware trade gets tired, the software trade gets a second look. That means the tools you use today—for writing, image generation, data analysis, customer support—are likely to see more investment, more competition, and more rapid improvement.

Lean into the shift. Pay attention to the tools that solve problems, not just the ones that boast parameter counts. Watch the platforms that are quietly embedding AI where you already work. And if you’re comparing AI tools, remember that the best tool isn’t the one with the most hype—it’s the one that fits your workflow without demanding a data center of its own.

The market’s attention is moving up the stack. Yours should too.

Comments (0) No comments yet

Want to join this discussion? Login or Register.

No comments yet. Be the first to share your thoughts!