The core problem: tax law moves, general AI lags

Professional tax research is not a trivia contest. It’s a moving target shaped by statutes, regulations, rulings, notices, and ongoing agency interpretation.

That matters because general AI tools are built for broad language tasks, not live legal authority. They can summarize what they’ve seen. They are much less reliable at telling you what controls right now.

The available context points to a timely example: the OBBBA. It introduced broad changes across the code, and related guidance has continued to develop. In a setting like that, an answer from even a few months ago may already be old news wearing a fresh interface.

Why consumer chatbots keep failing this use case

1. They often work from stale information

Tax law does not politely wait for model updates.

If a tool’s knowledge base predates recent legislation or new IRS and Treasury guidance, it may produce answers that were once reasonable and are now wrong. The nasty part is that the tone usually stays the same. No blinking red light. No “warning: this may have expired in the meantime.”

2. They struggle with citable authority

In tax research, an answer without authority is not really an answer. It’s a suggestion in a blazer.

Professionals need to trace conclusions back to primary sources such as:

- Internal Revenue Code sections

- Treasury regulations

- IRS rulings and notices

- Court decisions where relevant

General-purpose AI tools often summarize without showing the authority chain. And when they do surface citations, those citations may be incomplete, misapplied, or simply wrong.

3. They flatten the hierarchy of sources

A major tax research problem is not just finding information. It’s understanding what matters more.

Primary authority and secondary commentary do not carry the same weight. A regulation is not interchangeable with a blog post. A practitioner summary may be useful, but it does not outrank the actual source.

General AI tools tend to ingest everything as text first and legal hierarchy second, if at all. That is a bad habit in tax.

4. They offer confidence, not accountability

Consumer chatbots are optimized to answer. Professional research tools are expected to support defensible work.

That difference is bigger than it sounds. In tax practice, you need an audit trail, a source path, and a basis you can verify. “The chatbot said so” is not a research memo. It’s a career limiting phrase.

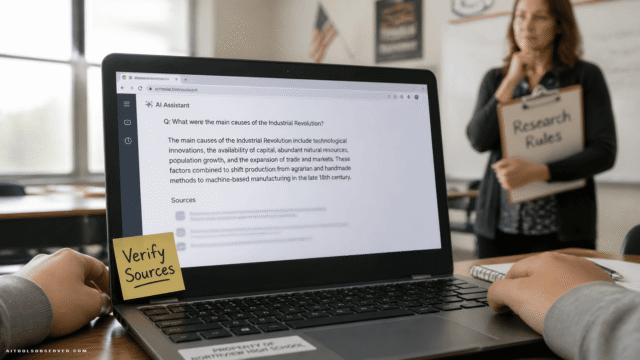

What hallucinations look like in tax research

Tax AI errors are usually not dramatic. They are sneaky.

More often, the model gives you something that looks plausible enough to pass a quick skim:

- a threshold from the wrong year

- a provision described without a later update

- a code section cited a little too loosely

- a sunset date that has already come and gone

- a transitional rule quietly ignored

That is exactly why this category is dangerous. The mistake does not need to be absurd to be costly. It just needs to be subtle enough to slip through.

Junior staff are especially exposed here. If you do not yet have the instincts to spot a shaky answer, polished language can feel like proof. It is not.

What professional-grade tax AI needs to do

If a tool is going to help with tax research, five things matter more than flashy chat UX.

Currency

The answer needs to reflect the current state of the law, including recent guidance.

Not “generally accurate.” Current.

Authority

Every conclusion should tie back to primary authority where applicable.

If the source path is fuzzy, the answer is too.

Context

Tax provisions do not live alone. They interact with phase-outs, effective dates, sunset rules, exceptions, and related sections.

A tool that cannot handle those interactions will produce tidy answers to messy questions. That’s not a compliment.

Consistency

Professionals need answers that are stable and reproducible.

If changing the prompt wording changes the legal position, that’s not research. That’s improv.

Expert curation

Open-web text is not the same thing as maintained professional content.

For tax work, the underlying material should be curated by subject-matter experts who understand source quality, authority weight, and what has been superseded.

So what should you use instead?

Based on the available context, the alternative is fiduciary-grade AI built for professional tax work rather than general conversation.

That phrase matters because it points to a higher standard: current, expert-curated, citable answers grounded in primary authority. Not merely fluent outputs.

The description specifically positions CoCounsel Tax this way. It appears designed to draw on expert-curated Checkpoint content and to return answers tied to authority that practitioners can actually verify.

Why that changes the outcome

The difference is not cosmetic. It changes the job the tool is doing.

A general chatbot tries to produce a likely answer from broad patterns in text. A fiduciary-grade research tool is supposed to produce a defensible answer from authoritative material.

In practice, that means:

- junior staff can get pointed to the right source, not just a likely-sounding explanation

- senior practitioners can move faster without losing the citation trail

- firms reduce the risk of confident-but-wrong output sneaking into client work

That last point is the quiet killer. Bad research rarely announces itself as bad research. It arrives dressed as efficiency.

The OBBBA effect: why this matters right now

The recent burst of tax law change makes the limits of general AI especially obvious.

When major provisions are changing, and agency guidance is still developing, the gap between “sounds right” and “is right under current authority” gets wider. A tool that cannot keep up with that environment becomes less useful exactly when the stakes get higher.

This is why broad AI works fine for some tasks and falls apart here. Tax research is not just information retrieval. It is authority-sensitive interpretation under changing rules.

General chatbots were not built for that. They were built to be helpful. Sometimes that’s the problem.

A practical rule of thumb

Use general AI for low-risk drafting, brainstorming, and first-pass organization.

Do not use it as the final word on live tax questions that require current law, source hierarchy, and citable authority. For that, use a tool positioned for professional research, such as fiduciary-grade tax AI.

Fast is good. Fast and unverifiable is how bad advice gets a head start.

Comments (0) No comments yet

Want to join this discussion? Login or Register.

No comments yet. Be the first to share your thoughts!